Bond — Growth

The path to GDP, not the stale print — core sub-metrics over headlines, nominal series deflated to real, and the consumer judged on whether spending is funded by income or by drawing down savings.

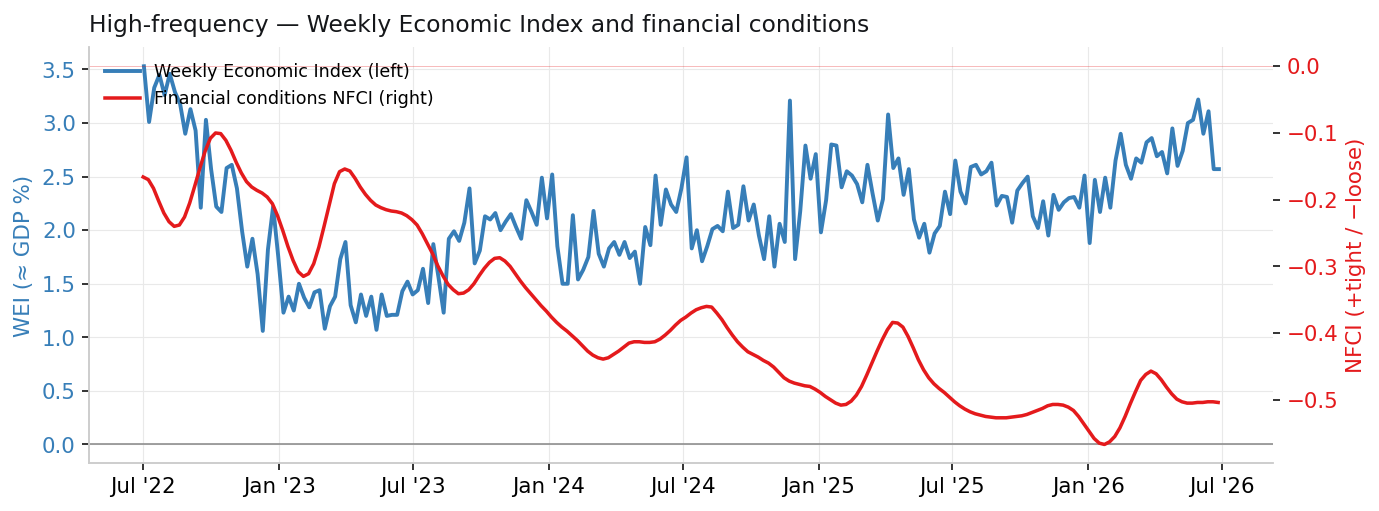

Updated 2026-07-05 08:36 KST · GDPNow 2026-04-01 · monthly through 2026-05-01 · weekly 2026-06-27 · source: FRED

Reads the path to GDP, not the stale quarterly print. Core sub-metrics over headlines (retail control group, core capex), nominal series deflated to real, and the consumer judged on sustainability — is spending funded by income or by drawing down savings. Soft-data leads hard. Licensed surveys not on FRED (ISM, S&P Global PMI, LEI, NAHB, NFIB) are crawled from their official releases into a local store.

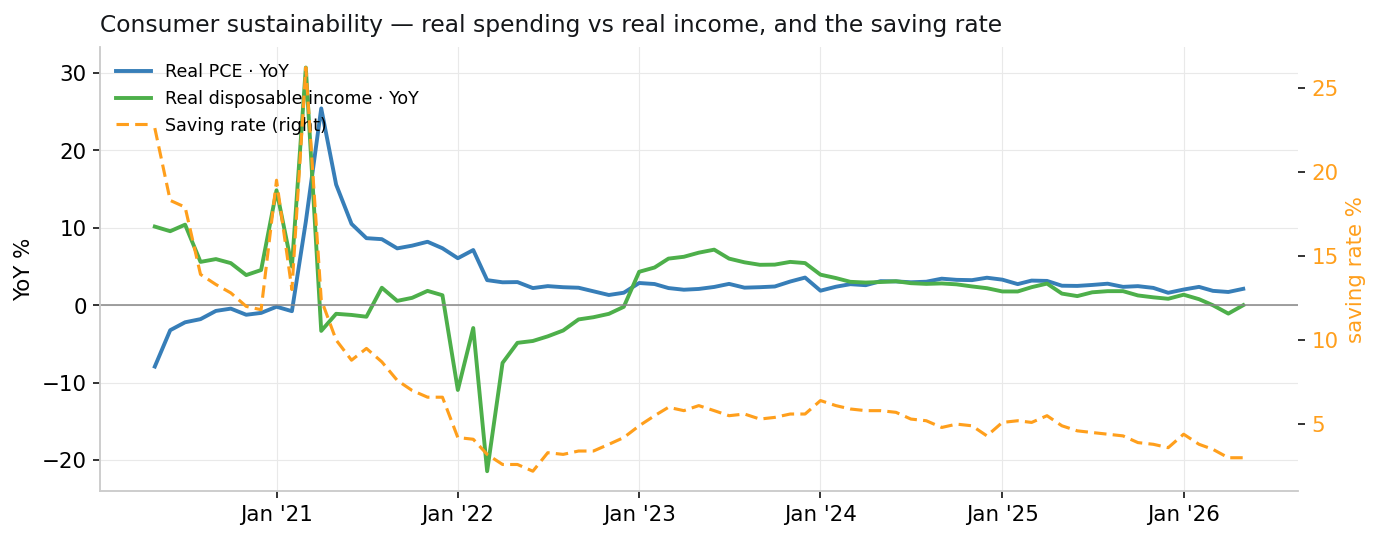

The consumer ~70% of GDP

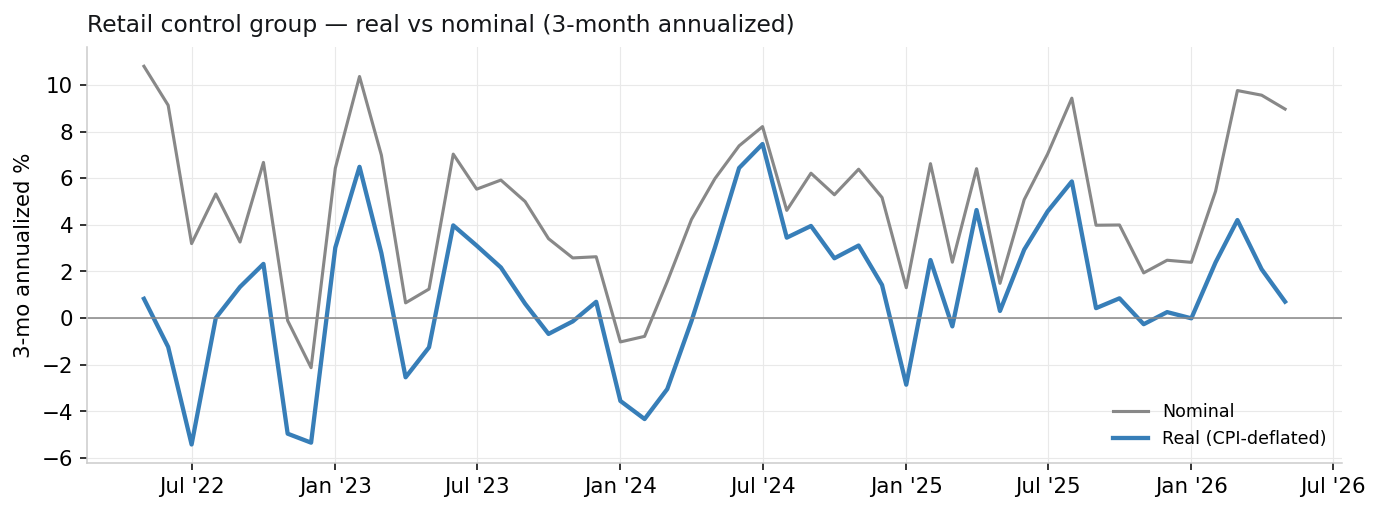

The control group strips out the noisy bits (autos, gas, building materials, restaurants). Watch the real read, not nominal — and whether spending is outrunning income.

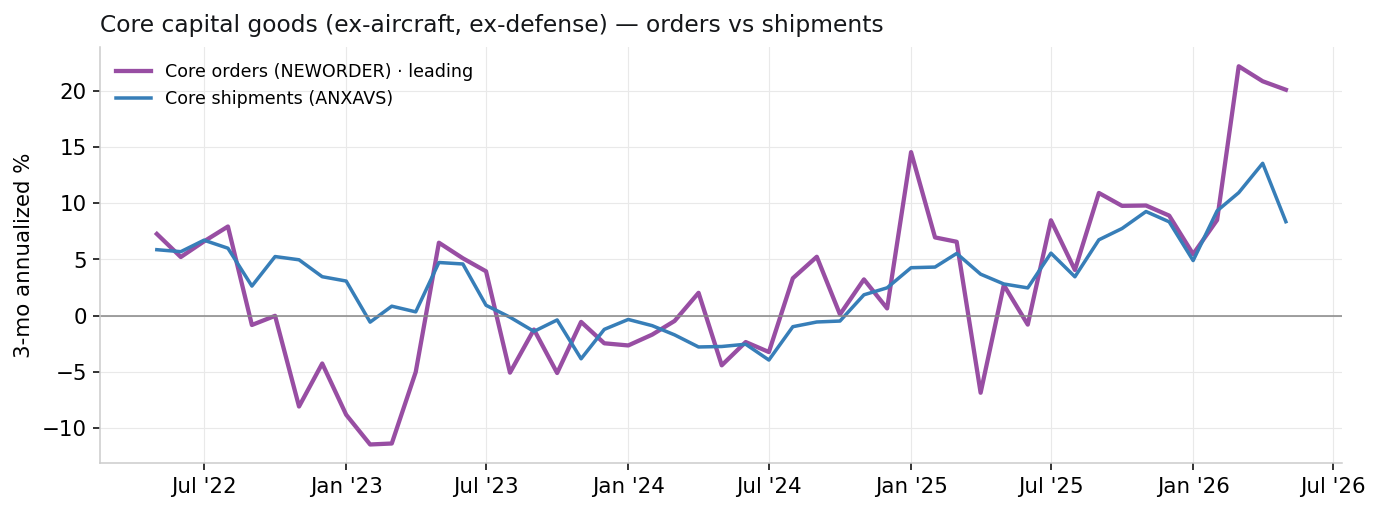

Business investment

Core capital goods — nondefense ex-aircraft — not the Boeing-dominated headline. Orders lead shipments.

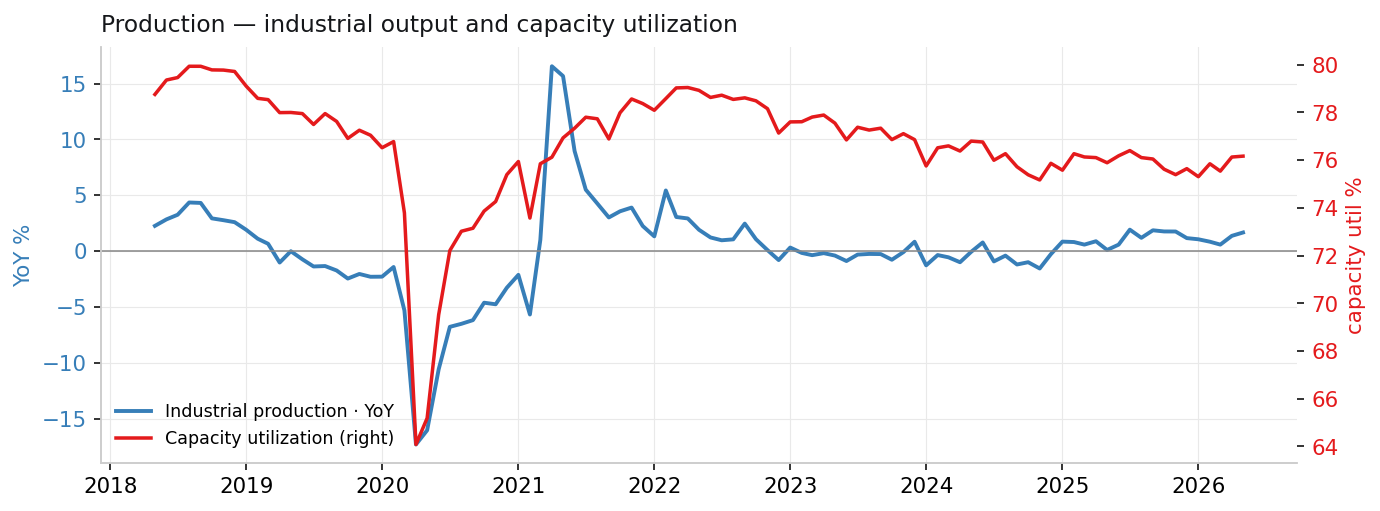

Production

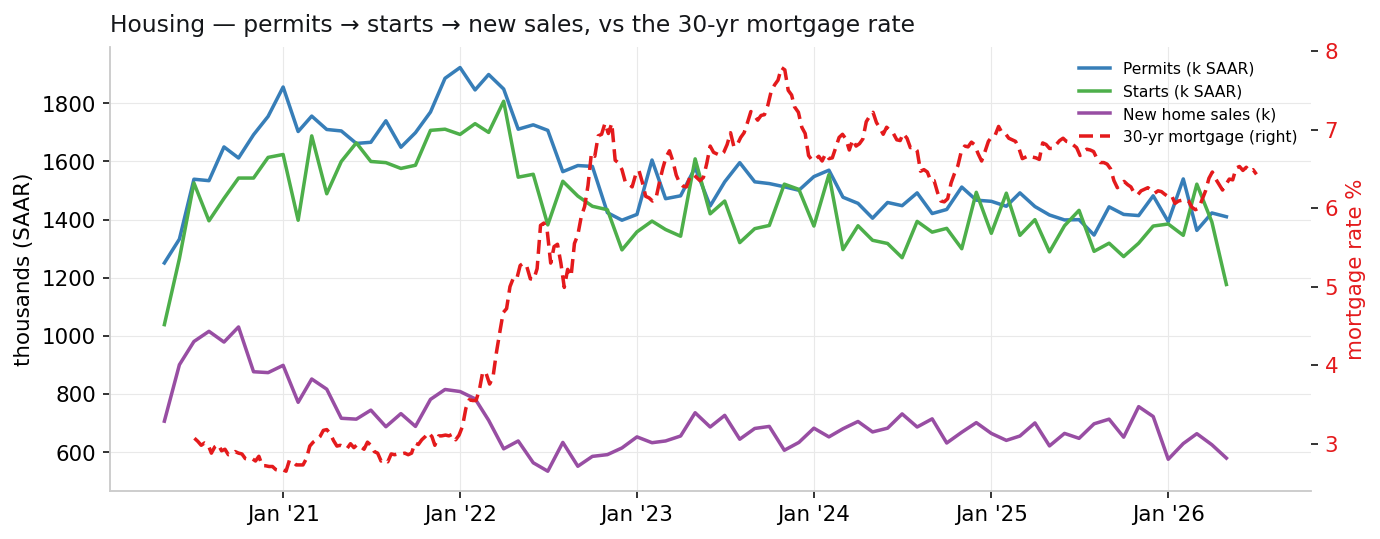

Housing leading cyclical

Read in lead order: permits → starts → new sales, driven by the mortgage rate.

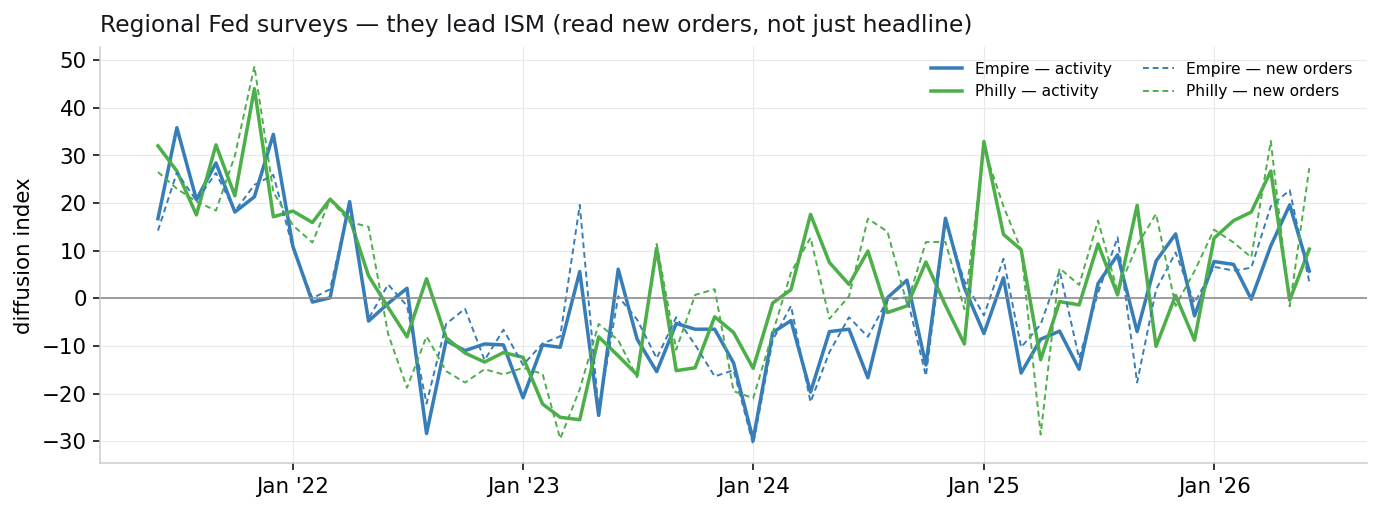

Soft-data leading edge

Regional Fed surveys (on FRED) lead ISM. Read the new-orders sub-component, not just the headline.

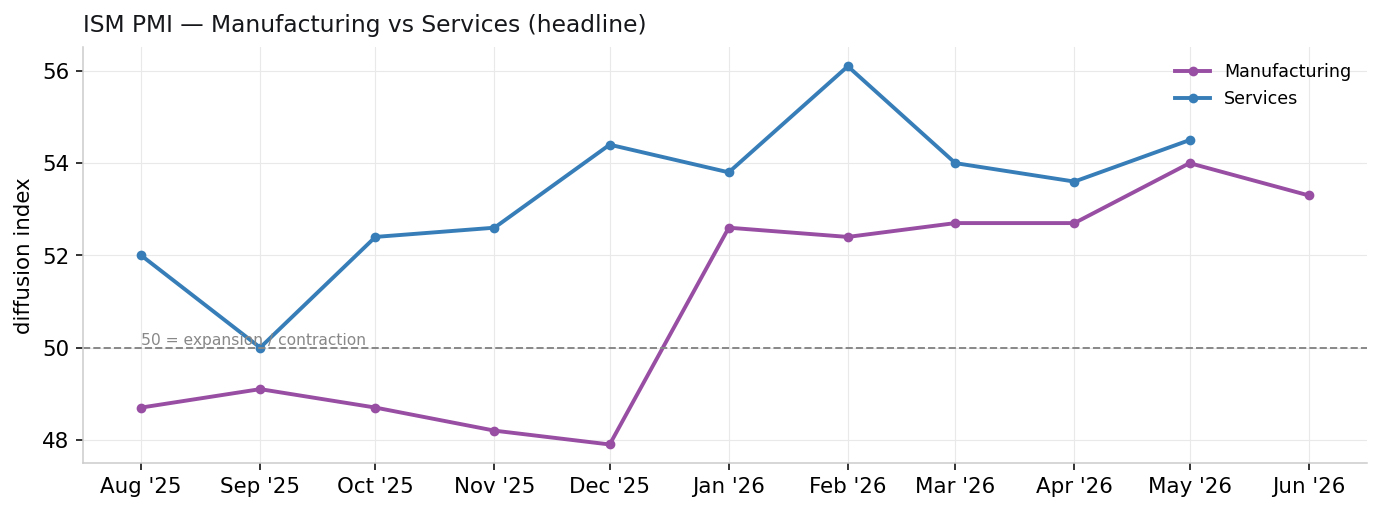

ISM PMI 2026-06-01 · crawled

Read New Orders (the leader) and Prices (early inflation). New Orders − Inventories is the cleanest forward tell. 50 = expansion threshold.

From ISM's Report On Business (via PRNewswire), stored locally. History accumulates monthly.

S&P Global US PMI 2026-05-01 · crawled

An independent survey from ISM (different panel/methodology) — a useful cross-check. Flash prints ~a week before the final and ~10 days before ISM. 50 = expansion.

Leading & sentiment

Conference Board LEI, builder (NAHB) and small-business (NFIB) sentiment, and Cass freight volumes — the forward-looking edge.

LEI / NAHB / NFIB crawled from their official releases and stored locally; Cass via FRED.

High-frequency