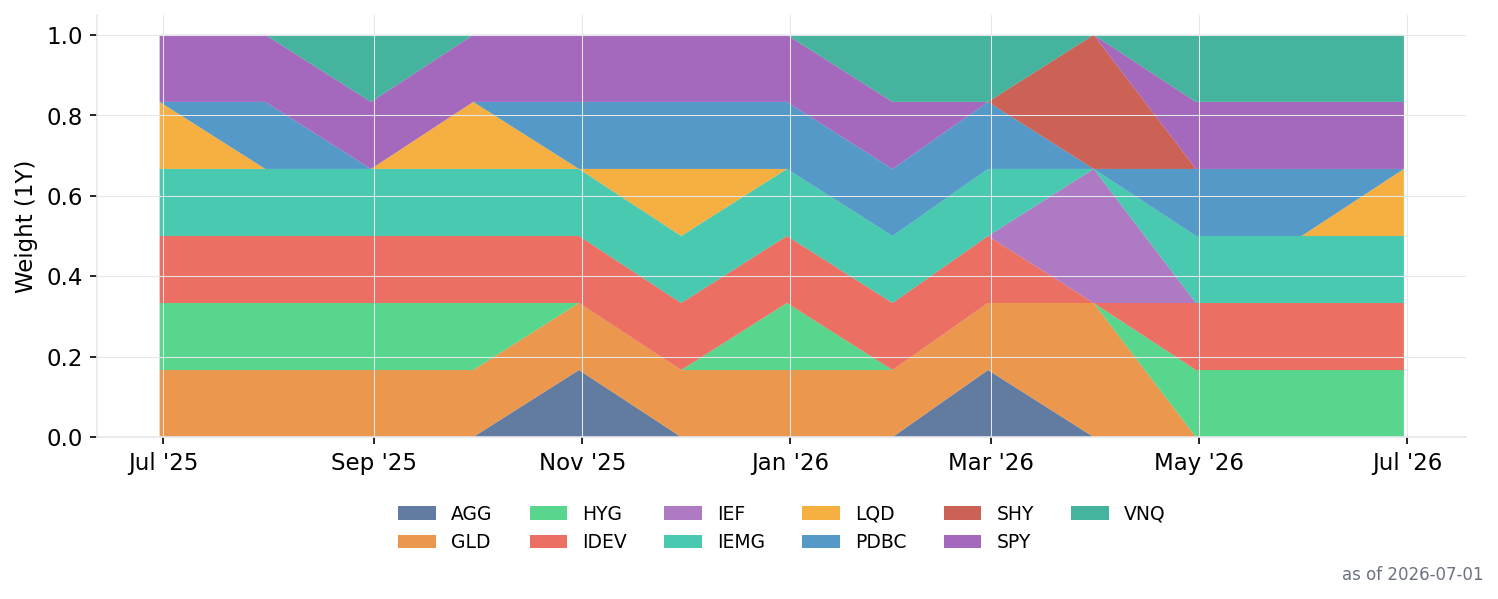

Canary / Crash-Protection AA

Current Allocation

| Category | Security | Ticker | Weight | vs prev month-end |

|---|---|---|---|---|

| Bond | iShares iBoxx HY Corp Bond | HYG | 16.7% | 0.0%p |

| Bond | iShares iBoxx IG Corp Bond | LQD | 16.7% | +16.7%p |

| Cash | Cash (SHY/T-bills) | Cash | 0.0% | 0.0%p |

| Equity | iShares Core MSCI Intl Developed | IDEV | 16.7% | 0.0%p |

| Equity | iShares Core MSCI Emerging Mkts | IEMG | 16.7% | 0.0%p |

| Equity | SPDR S&P 500 | SPY | 16.7% | 0.0%p |

| Real Asset | Vanguard Real Estate | VNQ | 16.7% | 0.0%p |

| Real Asset | Invesco Optimum Yield Commodity | PDBC | 0.0% | -16.7%p |

Weight change vs previous month-end rebalance (2026-05-31).

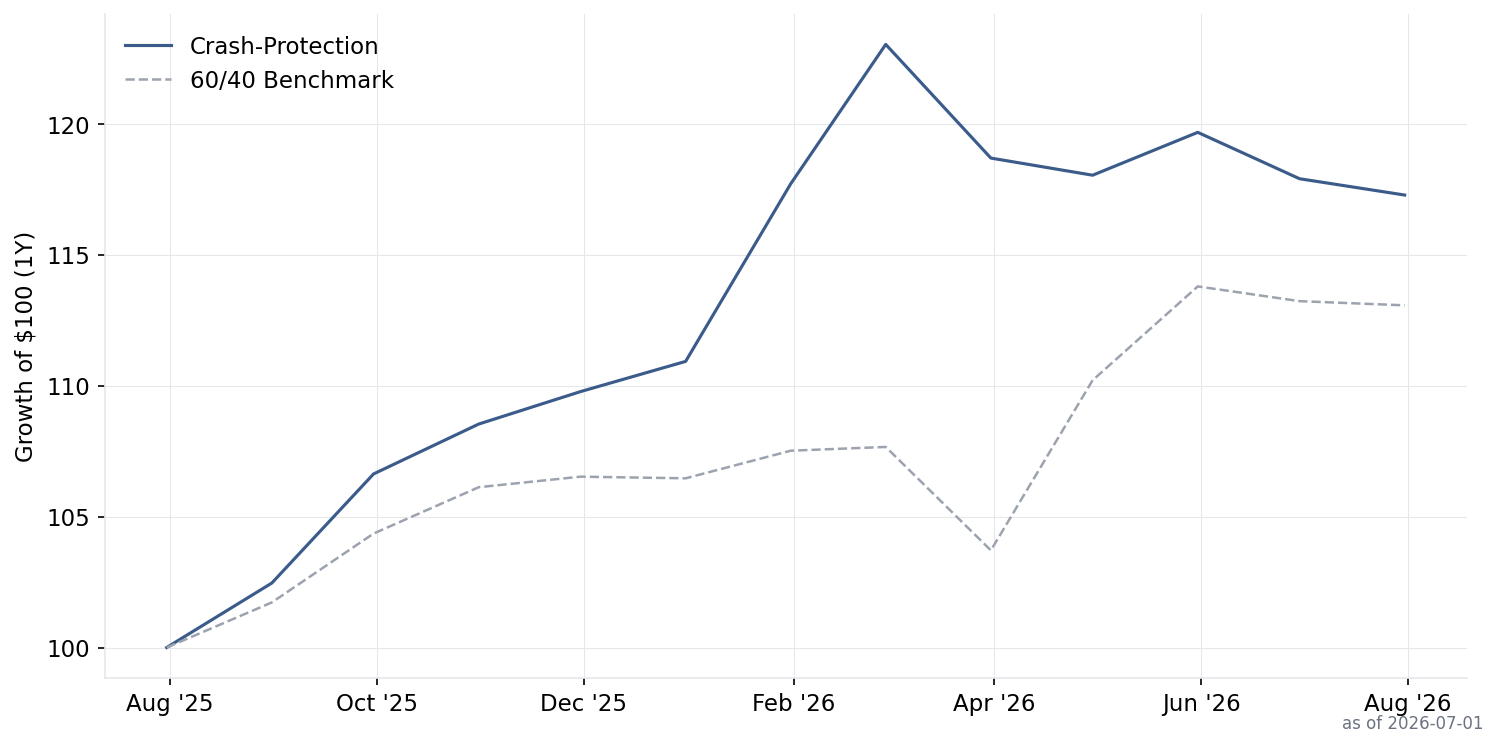

Performance vs 60/40

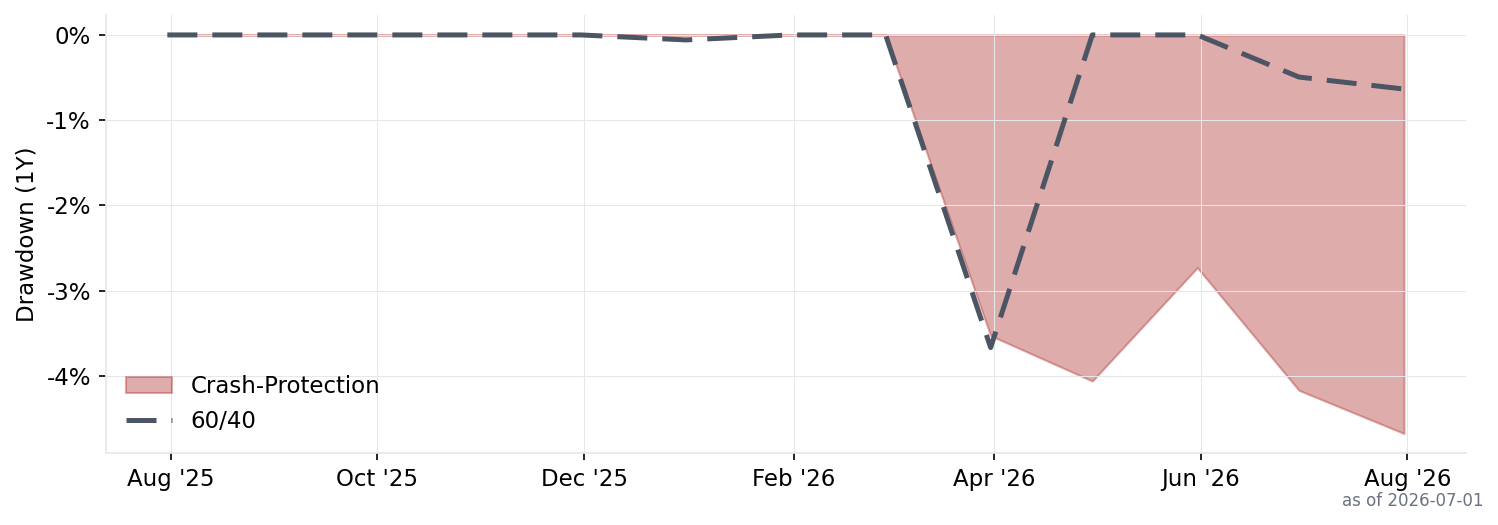

Drawdown

Allocation History

Latest month-end signals

Signals are evaluated once a month at month-end; they do not update intraday.

| Type | Security | Asset | Momentum | Signal | Signal Date |

|---|---|---|---|---|---|

| Canary | — | VWO | 1.31% | POSITIVE | 2026-07-31 |

| Canary | — | BND | 0.24% | POSITIVE | 2026-07-31 |

| Offensive | — | SPY | 2.66% | SELECTED | 2026-07-31 |

| Offensive | — | IEMG | 2.27% | SELECTED | 2026-07-31 |

| Offensive | — | VNQ | 2.14% | SELECTED | 2026-07-31 |

| Offensive | — | IDEV | 1.72% | SELECTED | 2026-07-31 |

| Offensive | — | HYG | 0.47% | SELECTED | 2026-07-31 |

| Offensive | — | LQD | 0.27% | SELECTED | 2026-07-31 |

| Defensive | — | SHY | 0.18% | SELECTED | 2026-07-31 |

| Defensive | — | IEF | -0.01% | SELECTED | 2026-07-31 |

| Defensive | — | GLD | -2.84% | SELECTED | 2026-07-31 |

Strategy Details

Wouter Keller & Jan Willem Keuning's Defensive Asset Allocation (DAA) from their 2018 paper. DAA uses "canary" assets — emerging market equities (VWO) and US aggregate bonds (BND) — as early-warning indicators. These assets tend to break down before US equities in a crisis. When canary momentum is positive, the portfolio goes fully offensive into the top-ranked risky assets. When canary signals turn negative, the portfolio proportionally shifts into defensive safe-haven assets. The key innovation is the 13612W momentum formula that heavily weights recent performance for faster signal detection.

Asset Universe

- Canary Assets (risk gauge)

- VWO (Emerging market equity), BND (US aggregate bonds)

- Offensive Assets

- SPY, IDEV, IEMG, AGG, LQD, HYG, VNQ, GLD, PDBC

- Defensive Assets

- IEF (7-10Y Treasuries), SHY (short-term Treasuries), GLD (Gold)

Scoring Formula

Momentum Score (13612W) = (12 × 1M return + 4 × 3M return + 2 × 6M return + 1 × 12M return) / 19 — heavily front-weighted for fast regime detection

Decision Rules

- Calculate 13612W momentum for canary assets (VWO, BND)

- If ALL canary momentum ≥ 0 → full offensive: equal-weight top 6 of 9 offensive assets by momentum

- If ANY canary momentum < 0 → proportional shift: B/2 fraction to defensive (B = number of bad canary signals)

- Defensive allocation: equal-weight top 3 defensive assets by momentum

- Offensive remainder: top 6 offensive assets by momentum

Source

Wouter Keller & Jan Willem Keuning, 'Defensive Asset Allocation (DAA)', 2018 — Paper

Caveats

- IEMG data starts 2012-10-24, limiting backtest history.

- PDBC data starts 2014-11-07, limiting backtest history.

- IDEV data starts 2017-03-23, limiting backtest history.

- HYG data starts 2007-04-11, limiting backtest history.

- BND data starts 2007-04-10, limiting backtest history.

- VWO data starts 2005-03-10, limiting backtest history.

Data: Alpha Vantage (prices), FRED (unemployment). Transaction cost: 5bps/trade. Backtest: 2017-03-31 to 2026-07-01. Generated: 2026-07-02 09:30:55.