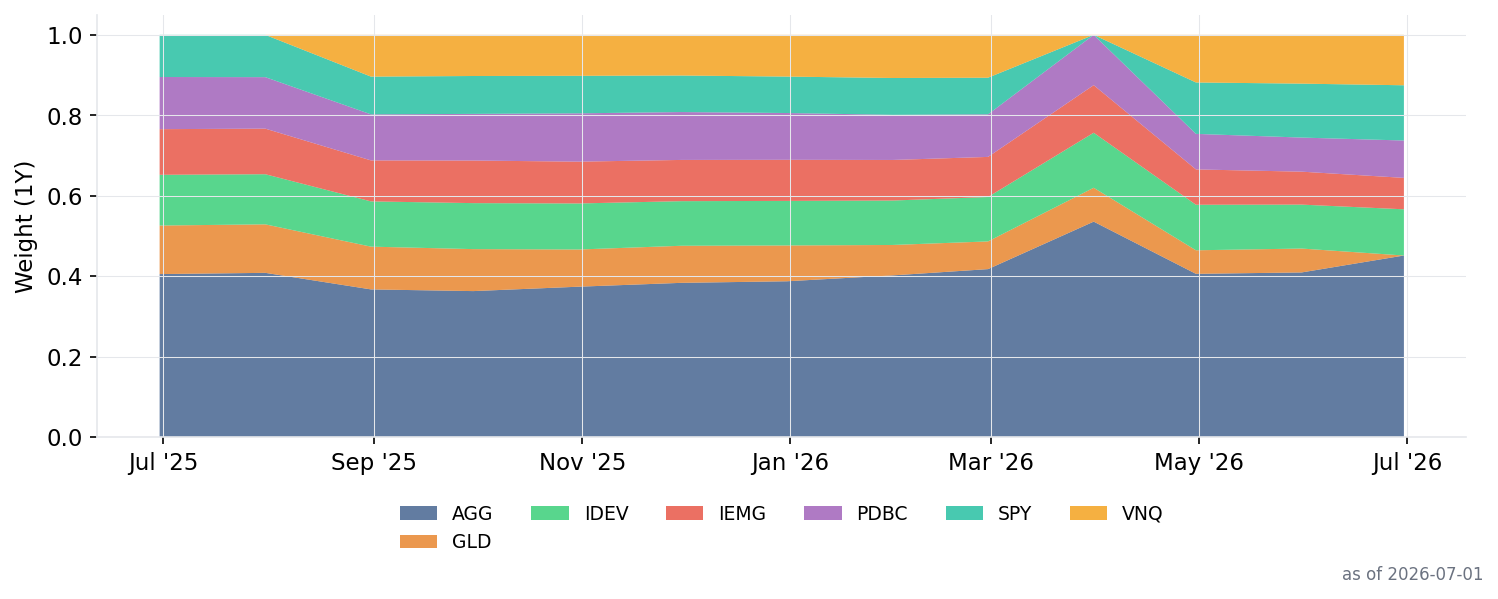

Risk-Parity Trend-Following AA

Current Allocation

| Category | Security | Ticker | Weight | vs prev month-end |

|---|---|---|---|---|

| Bond | iShares Core US Agg Bond | AGG | 45.1% | +4.2%p |

| Cash | Cash (SHY/T-bills) | Cash | 0.0% | 0.0%p |

| Equity | SPDR S&P 500 | SPY | 13.7% | +0.3%p |

| Equity | iShares Core MSCI Intl Developed | IDEV | 11.5% | +0.6%p |

| Equity | iShares Core MSCI Emerging Mkts | IEMG | 7.8% | -0.4%p |

| Real Asset | Vanguard Real Estate | VNQ | 12.5% | +0.4%p |

| Real Asset | Invesco Optimum Yield Commodity | PDBC | 9.3% | +0.8%p |

| Real Asset | SPDR Gold Shares | GLD | 0.0% | -5.9%p |

Weight change vs previous month-end rebalance (2026-05-31).

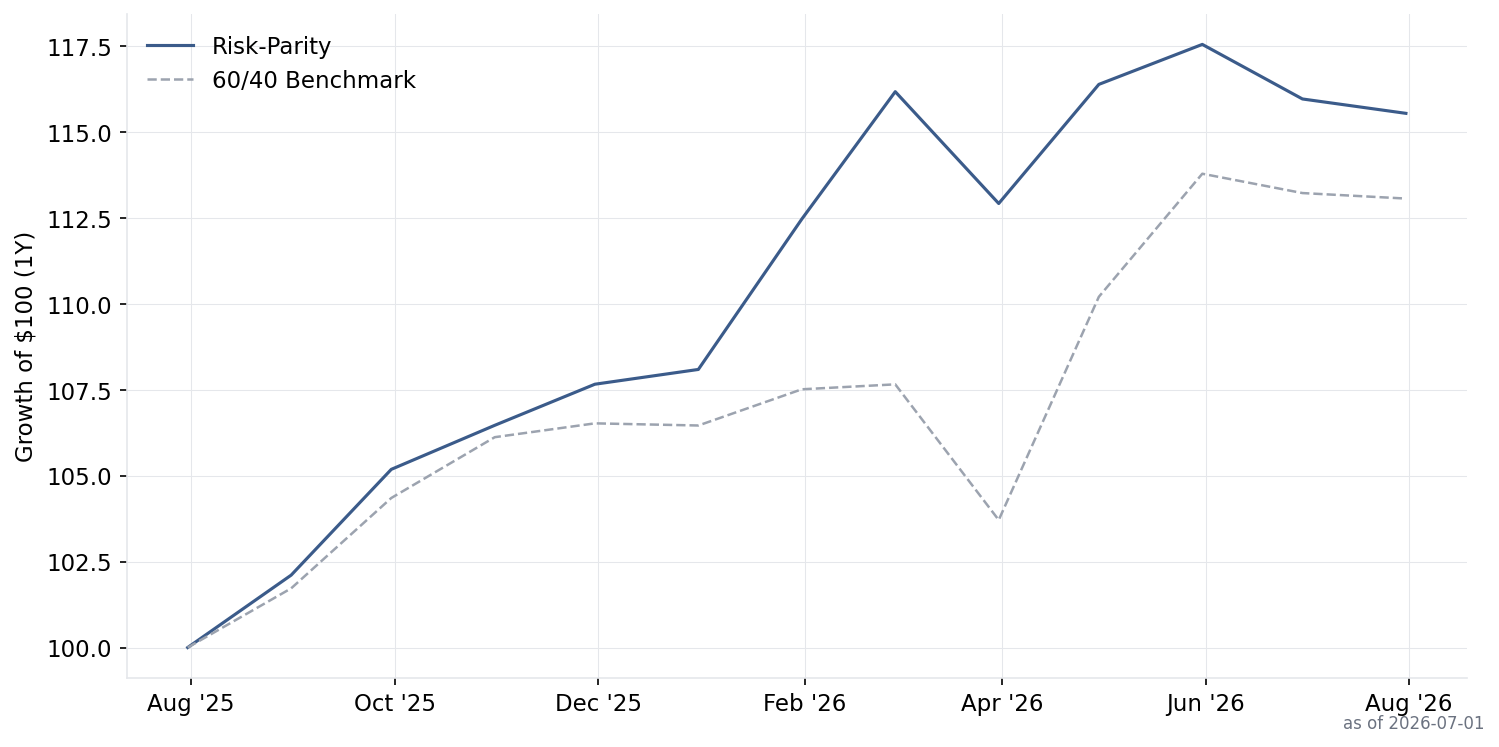

Performance vs 60/40

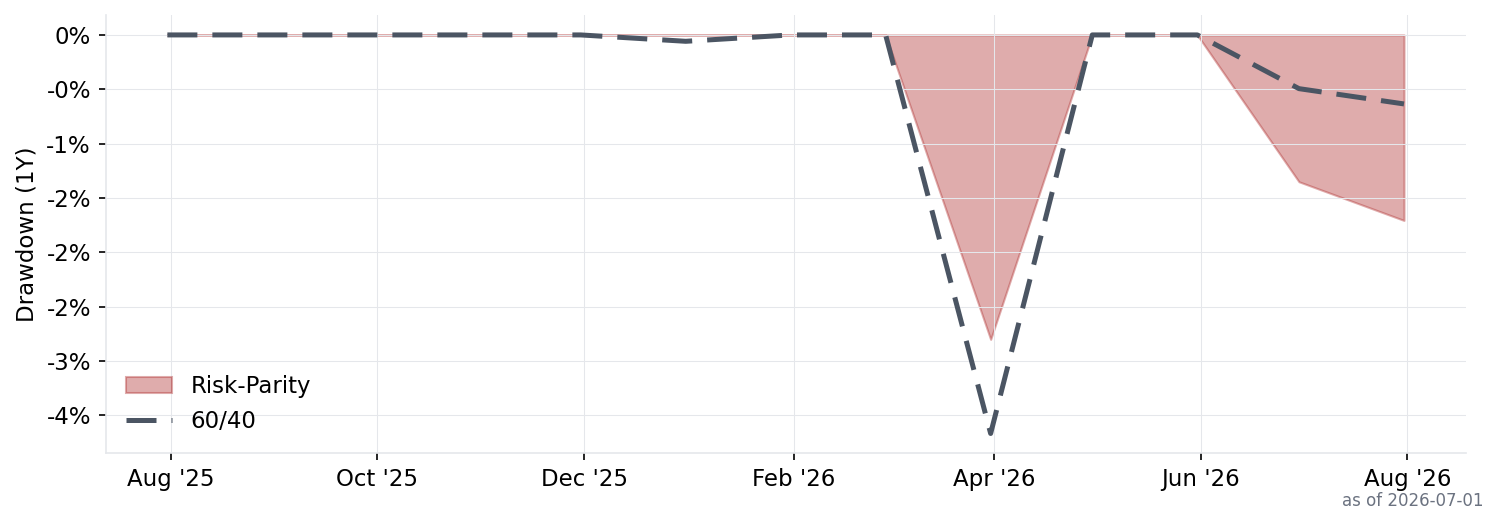

Drawdown

Allocation History

Latest month-end signals

Signals are evaluated once a month at month-end; they do not update intraday.

| Asset | Security | Price | SMA10M | Vol252 | Trend | Signal Date |

|---|---|---|---|---|---|---|

| SPY | SPDR S&P 500 | 745.76 | 701.58 | 12.5% | ON | 2026-07-31 |

| IDEV | iShares Core MSCI Intl Developed | 88.61 | 84.88 | 15.0% | ON | 2026-07-31 |

| IEMG | iShares Core MSCI Emerging Mkts | 80.63 | 74.03 | 22.2% | ON | 2026-07-31 |

| AGG | iShares Core US Agg Bond | 98.5 | 98.32 | 3.8% | ON | 2026-07-31 |

| VNQ | Vanguard Real Estate | 96.82 | 91.66 | 13.7% | ON | 2026-07-31 |

| GLD | SPDR Gold Shares | 370.6 | 409.11 | 27.7% | OFF | 2026-07-31 |

| PDBC | Invesco Optimum Yield Commodity | 15.78 | 15.41 | 18.6% | ON | 2026-07-31 |

Strategy Details

Based on Clare, Seaton, Smith & Thomas's 2012 paper "The Trend is Our Friend." Classic risk parity weights assets by inverse volatility so each contributes roughly equal risk to the portfolio. This version adds a trend filter: assets that fall below their 10-month SMA are excluded and their allocation moves to cash. The combination of risk-parity weighting and trend filtering aims to reduce drawdowns during bear markets while maintaining diversified exposure during normal times. Lower-volatility assets (bonds, gold) naturally receive larger allocations.

Asset Universe

- Risk Assets

- SPY (US equity), IDEV (Int'l developed), IEMG (Emerging markets), AGG (US bonds), VNQ (REITs), GLD (Gold), PDBC (Commodities)

- Cash

- SHY (US short-term Treasuries)

Scoring Formula

Weight = (1 / 252-day trailing volatility) — normalized across trend-positive assets only

Decision Rules

- Calculate 252-day (1-year) annualized trailing volatility for each asset

- Trend filter: only include assets with price > 10-month SMA

- Weight trend-positive assets by inverse volatility (equal risk contribution)

- Assets failing the trend filter → allocation goes to cash (SHY)

- If all assets fail trend → 100% cash

Source

Clare, Seaton, Smith & Thomas, 'The Trend is Our Friend: Risk Parity, Momentum and Trend Following in Global Asset Allocation', 2012 — Paper

Caveats

- IEMG data starts 2012-10-24, limiting backtest history.

- PDBC data starts 2014-11-07, limiting backtest history.

- IDEV data starts 2017-03-23, limiting backtest history.

Data: Alpha Vantage (prices), FRED (unemployment). Transaction cost: 5bps/trade. Backtest: 2017-03-31 to 2026-07-01. Generated: 2026-07-02 09:30:55.