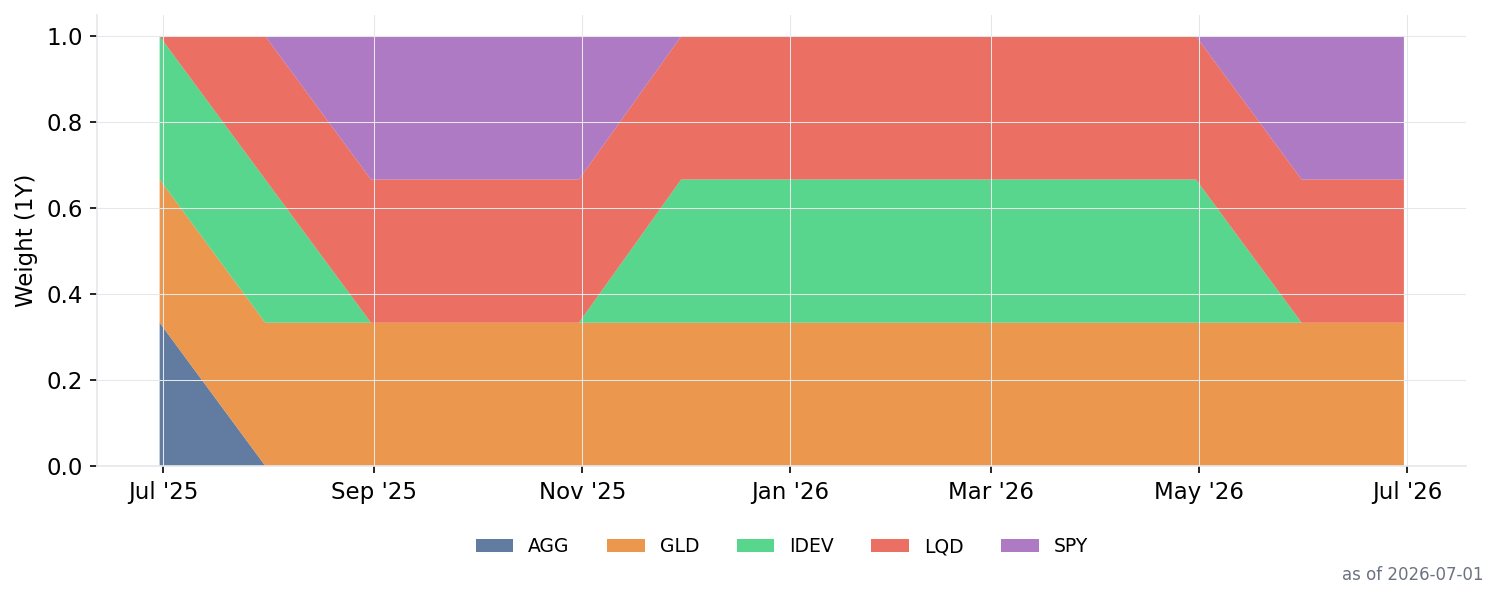

Dual Momentum AA

Current Allocation

| Category | Security | Ticker | Weight | vs prev month-end |

|---|---|---|---|---|

| Bond | iShares iBoxx IG Corp Bond | LQD | 33.3% | 0.0%p |

| Cash | Cash (SHY/T-bills) | Cash | 0.0% | 0.0%p |

| Equity | SPDR S&P 500 | SPY | 33.3% | 0.0%p |

| Real Asset | SPDR Gold Shares | GLD | 33.3% | 0.0%p |

Weight change vs previous month-end rebalance (2026-05-31).

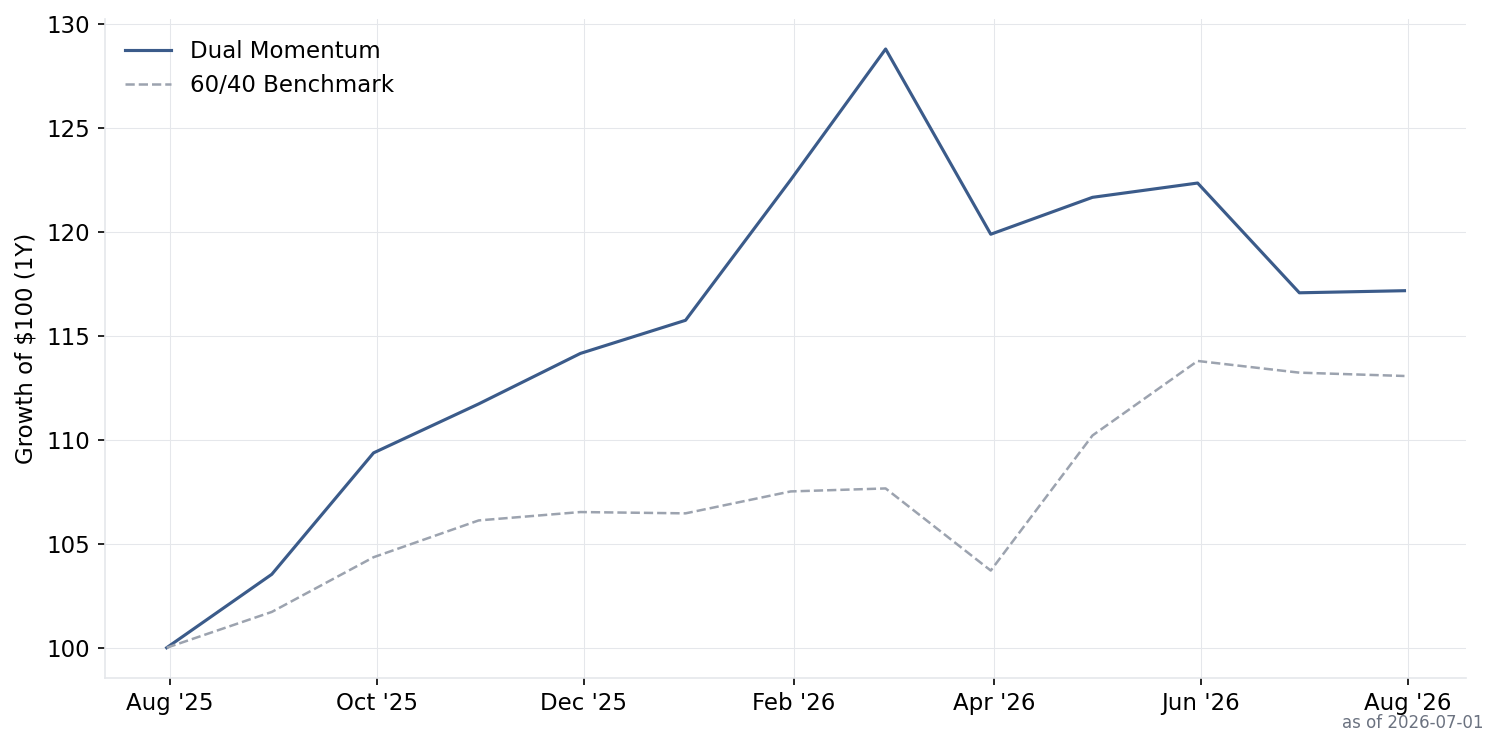

Performance vs 60/40

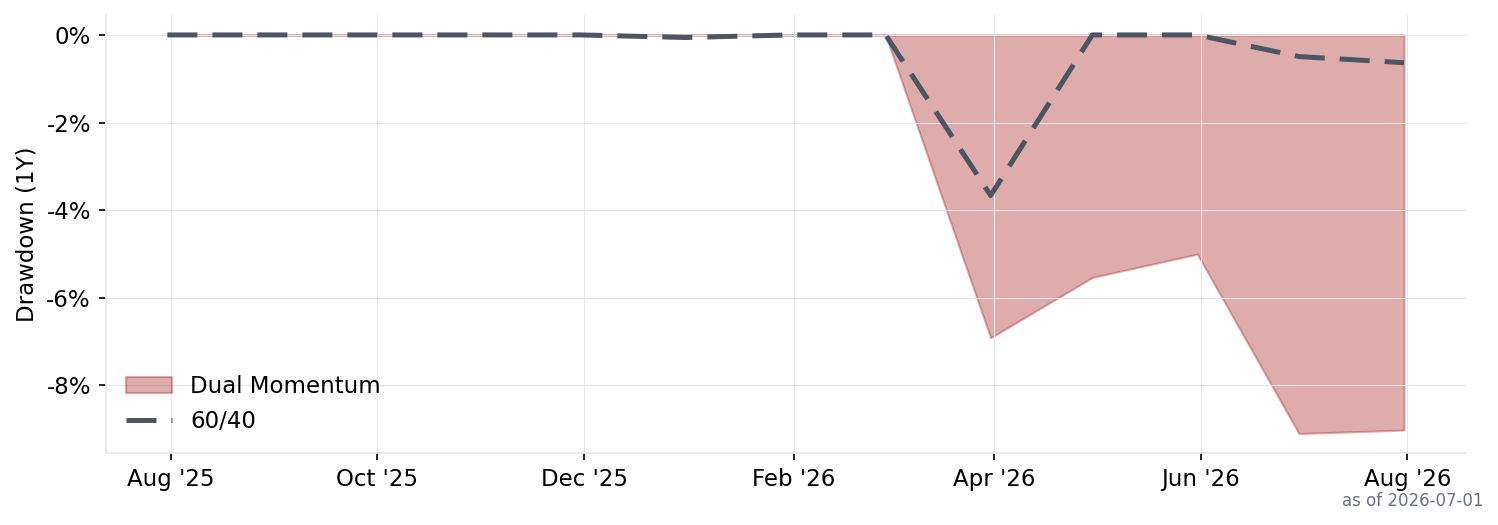

Drawdown

Allocation History

Latest month-end signals

Signals are evaluated once a month at month-end; they do not update intraday.

| Sleeve | Security | Asset A | Asset B | Winner | Abs Mom | Holding | Signal Date |

|---|---|---|---|---|---|---|---|

| Equities | — | SPY (22.2%) | IDEV (21.0%) | SPY | 22.2% | SPY | 2026-07-31 |

| Bonds | — | AGG (3.8%) | LQD (4.1%) | LQD | 4.1% | LQD | 2026-07-31 |

| Real Assets | — | VNQ (12.5%) | GLD (20.8%) | GLD | 20.8% | GLD | 2026-07-31 |

Strategy Details

Gary Antonacci's Dual Momentum strategy combines two types of momentum: relative momentum (which asset is stronger?) and absolute momentum (is the winner even going up?). The portfolio is split into three sleeves — equities, bonds, and real assets. Within each sleeve, the stronger of two assets is selected, but only if its 12-month return is positive. If not, the sleeve defaults to a safe asset. This dual filter avoids holding assets with good relative but bad absolute performance.

Asset Universe

- Equities Sleeve

- SPY (US equity) vs. IDEV (Int'l developed) → safe: AGG (US bonds)

- Bonds Sleeve

- AGG (US bonds) vs. LQD (US corp bonds) → safe: SHY (short-term Treasuries)

- Real Assets Sleeve

- VNQ (REITs) vs. GLD (Gold) → safe: SHY

Scoring Formula

Momentum Score = 12-month total return (skipping the most recent month to avoid reversal noise)

Decision Rules

- Split portfolio into 3 equal sleeves (1/3 each): equities, bonds, real assets

- Within each sleeve: rank the two risky assets by 12-month return (skip last month)

- Relative momentum: pick the winner

- Absolute momentum filter: only hold the winner if its 12M return > 0

- If absolute momentum fails → hold the sleeve's safe asset

Source

Gary Antonacci, 'Dual Momentum Investing', 2014 / 'Risk Premia Harvesting Through Dual Momentum' — Paper

Caveats

- IDEV data starts 2017-03-23, limiting backtest history.

Data: Alpha Vantage (prices), FRED (unemployment). Transaction cost: 5bps/trade. Backtest: 2017-03-31 to 2026-07-01. Generated: 2026-07-02 09:30:54.